Jaké jsou kategorie pro emise dluhopisů? Jaká kritéria je nutné posuzovat při investičním rozhodování a co jsou další investiční alternativy? Na tyto a další otázky vám odpoví tento článek.

Historicky nejnižší úrokové sazby a jejich vliv na dluhopisy

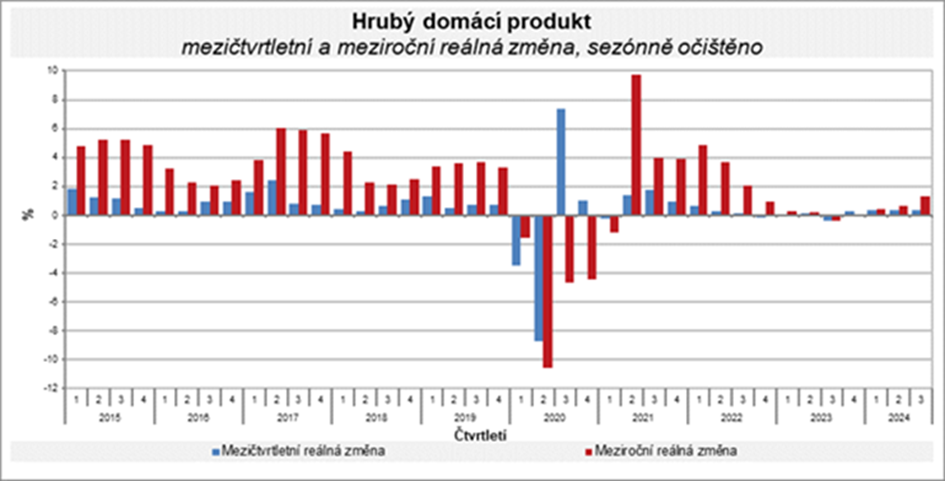

V letech 2018–2020 bylo za extrémně nízkých, a do budoucna sotva opakovatelných, úrokových sazeb vydáno velké množství dluhopisů. Tehdy, vzhledem k nulovým úrokovým sazbám, byl velký zájem drobných investorů o korporátní dluhopisy a řada firem toho v dobré víře využila. Vzhledem k časté době splatnosti kolem 5 let dochází nyní k jejich splatnosti.

V business plánech sestavených v době emise se logicky nepočítalo s nečekaně vysokou mírou inflace, téměř nulovým růstem HDP České republiky, globálním makroekonomickým a geopolitickým vývojem a odpovídajícím ekonomickým vývojem v České republice.

Vývoj HDP od roku 2015 dle Českého statistického úřadu.

Rizika nezajištěných firemních dluhopisů

Firemní dluhopisy jsou mezi menšími investory často vyhledávány pro své potenciálně zajímavé výnosy a investoři je plánují držet až do jejich splatnosti.

Mnoho investorů chybně předpokládá, že dluhopisy jsou automaticky garantované či zajištěné, díky čemuž nemohou přinést investorovi ztrátu. Investice do dluhopisů totiž stále nese rizika, především kreditní (bonita emitenta) a úrokové (citlivost ceny na sazby). Celkově platí, že i firemní dluhopisy jsou investice s určitými riziky. Proto je důležité, aby investoři pečlivě zvažovali své možnosti a byli si vědomi všech rizik spojených s investováním do dluhopisů

Na co si dát pozor před investicí do dluhopisů?

- Nabídka na první pohled působí mimořádně výhodně —například garantuje velmi vysoký výnos i nad 10 % p. a. — měl by investor zpozornět.

- Finančně slabší či netransparentní emitent, který nezveřejňují výsledky nad rámec povinných zpráv, obvykle nabízí výrazně vyšší výnosy než trh.

- Emitent dluhopisu, na kterého se nevztahuje ze zákona povinnost auditu, audit dobrovolně neprovádí nebo nezveřejní jeho výsledky.

- Investor nemá k dispozici dokumenty shrnující emisní podmínky a prospekt pro nákup korporátních dluhopisů v emisní hodnotě nad 25 mil. Dokumentace musí být po administrativní stránce schválena ČNB. Může obsahovat ustanovení zvyšující rizikovost příslušných dluhopisů jako je úpadek emitenta či podmínky splatnosti. Schválení ze strany ČNB však nezohledňuje rizikový profil emitenta ani schopnost dluhopis řádně splatit.

- Zvýšenou pozornost věnujte u dluhopisů v emisní hodnotě do 25 mil. Ty nepodléhají žádné regulaci. Emitent nemusí z regulatorních důvodů vydat nic, nikoho o nic nežádat. Defacto pouze připraví materiály jako prodejní nástroj, kterými by zároveň pokryl očekávané otázky investorů.

- Komunikační materiály obsahují termíny jako “Garantováno ČNB” atp.

Informace, že ČNB schválila emisi dluhopisů, znamená pouze to, že ČNB ověřila, zda prospekt příslušné dluhopisové emise splňuje všechny zákonem stanovené náležitosti, a poskytuje tak investorům dostatek informací pro jejich vlastní posouzení a rozhodnutí.

Dluhopis je investiční nástroj, kde investor má předem daný omezený zisk, ale nese neomezené riziko v případě úpadku emitenta. Vždy je lepší být obezřetný a informovaný než se nechat unést lákavými nabídkami dluhopisů.

Investiční alternativy – vyšší zhodnocení, nižší rizika

Pokud hledáte investici s nízkou mírou rizika a stabilním výnosem, tak jednou z investičních variant je Salutem Fund – fond kvalifikovaných investorů je primárně zaměřen na rezidenční nemovitosti držené ve svém portfoliu, které vykazují vyšší odolnost vůči ekonomickým výkyvům a umožňují získat výnos jak z prodeje, tak z pronájmu.

Salutem Fund je lépe připraven čelit nečekaným ekonomickým změnám díky stabilitě a reálné hodnotě nemovitostí v portfoliu, a také díky jejich typové a geografické diverzifikaci. Fond neúčtuje žádný manažerský poplatky ani žádné jiné skryté poplatky ukrajující investorovi ze zisku. Současné nastavení znamená, že fond nejdříve vydělá investorovi a teprve pak sám sobě.

- Ve své třídě akcií PIA fond investorům nabízí roční výnos 6,3 % až 7,0 %, uvedených 6,3 % i v případě horšího výsledku fondu.

- Preferované výnosy jsou zajištěny zakladateli fondu vlastním kapitálem, třídou akcií VIA. Zakladatelé navíc začnou vydělávat až v momentě, kdy jsou uspokojeny nároky investorů – držitelů prioritních investičních akcií PIA. V současné době je poměr objemu akcií VIA x PIA přibližně 8,5: 1.

Stabilita fondu je dána i jeho nízkým zadlužením, celkové závazky fondu činí pouze třetinu jeho aktiv.

Ve srovnání s emitentem dluhopisů Salutem Fund podléhá přísnému dohledu nezávislých institucí a povinnosti zveřejňovat výsledky svého hospodaření.

Obhospodařovatel fondu, TILLER, investiční společnost, a.s. je povinen čtvrtletně zveřejňovat své hospodářské výsledky fondu. Spolu s tím Salutem Fund ze zákona podléhá povinnosti auditu hospodářských výsledků. Salutem Fund si jako auditora vybral společnost Audit One s.r.o., která je členskou firmou společnosti CLA Global.

Složené úročení vs. fixní kupónové platby

Držitel dluhopisů inkasuje svůj výnos pravidelně, a nemá možnost využít složeného úročení. Naopak v případě Salutem Fund je zvyšování výnosů složeným úročením jeho základním principem. U třídy PIA to vede k výnosům:

- 20,1 % – 22,5 % za 3 roky

- 35,7 % – 40,2 % za 5 let

Navíc jsou výnosy z akcií PIA po 3 letech držení při jejich prodeji do částky 40 milionů korun osvobozeny od daně z příjmu fyzických osob, na rozdíl od úroků z dluhopisů, které podléhají 15% srážkové dani. Výnosu fondu 6,3 % p. a. odpovídá výnos dluhopisu 7,4 % o složeném úročení navíc ani nemluvě (před podáním daňového přiznání k potřeba nechat si toto ověřit daňovým poradcem).

Flexibilní vs. fixní investiční horizont

Doba držení akcií fondu je časově neomezená, zatímco doba držení dluhopisu je dána termínem jeho splatnosti. I když by investor měl o inkasované úroky zájem i nadále, není to možné. Naopak v případě fondu závisí doba držení jeho akcií pouze na individuálním rozhodnutí investora a není nijak časově omezena.

Likvidita

Jak píšeme výše, investoři ve velké většině případů plánují držet firemní dluhopisy až do jejich splatnosti. jestliže je potřebují z jakýchkoliv důvodů prodat, obvykle se dostanou do problému, neboť neví komu a emitent dluhopisu není povinen je od nej odkoupit.

V případě Salutem Fund však investor má garantovaný odkup jeho akcií nezávisle ne tom, jak dlouho akcie fondu držel.

Celkové porovnání fondu s dluhopisy

| Salutem Fund – PIA | Dluhopis | |

| Fixní zaručený výnos (nad 1 rok) | ✅ | ✅ |

| Likvidní produkt (do 1 roku) | ✅ | ❌ |

| Bez výstupních poplatků | ✅ | ✅ |

| Bez časové náročnosti | ✅ | ❌ |

| Bez průběžných nákladů | ✅ | ✅ |

| Flexibilní investiční horizont | ✅ | ❌ |

| Daňové zvýhodnění | ✅ | ❌ |

| Míra bezpečí | Vysoká | Střední |

| Forma zajištění | Třída akcií VIA | Žádná |

Investice do Salutem Fund – třída akcií PIA – představuje výhodnější alternativu pro nákup dluhopisů, a to jak z pohledu výnosu, tak rizika.

Vyšší zhodnocení se Salutem Fund

Salutem Fund nabízí také investiční třídu akcií PRIA, nabízející vyšší růstový, avšak negarantovaný, výnos. Strategie fondu je dosahovat výnosnosti 15 % ročně, což by pro investora, který drží akcie PRIA, znamenalo zhodnocení 12,2 % ročně, resp. 77,8 % po 5ti letech.

??

The Ups and Downs of Bonds: What to Watch Out For and What Are Your Investment Alternatives?

What types of bonds are out there? What should you consider when making investment decisions, and what other investment options are available? This article will answer these and other questions for you.

Historically Low Interest Rates and Their Impact on Bonds

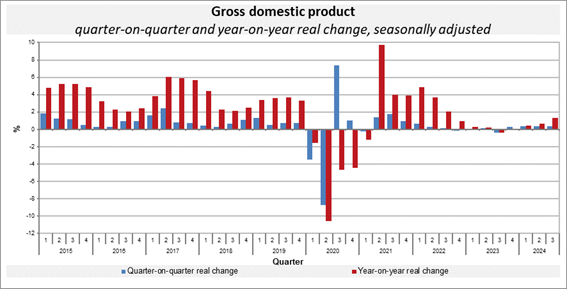

Between 2018 and 2020, a higher number of bonds were issued at extremely low interest rates, that we’re probably not going to see again anytime soon. Back then, with interest rates at zero, small investors were really into corporate bonds, and a lot of companies took advantage of that in good faith. Now, since many of these bonds had maturities of around five years, they’re starting to come due.

The business plans put together when these bonds were issued didn’t, of course, plan for unexpectedly high inflation, almost zero GDP growth in the Czech Republic, global macroeconomic and geopolitical shifts, and the related economic trends.

Risks of Unsecured Corporate Bonds

Corporate bonds are often popular among smaller investors because they can offer potentially attractive returns, and people plan to hold onto them until they mature.

Many investors mistakenly assume that bonds are automatically guaranteed or secured, so they think they can’t lose money on them. But investing in bonds still carries risks, mainly credit risk (the issuer’s creditworthiness) and interest rate risk (how sensitive the price is to rate changes). So, even corporate bonds are investments with certain risks That’s why it’s important for investors to carefully consider their options and be aware of all the risks associated with investing in bonds.

What to Watch Out For Before Investing in Bonds

- If an offer looks amazingly good at first glance—like guaranteeing a very high return over 10% per year—you should be on alert.

- Weaker or less transparent companies that don’t publish results beyond what’s required usually offer returns much higher than the market average.

- The bond issuer isn’t legally required to have an audit, doesn’t do one voluntarily, or doesn’t share the results.

- If investor doesn’t have access to documents summarizing the bond terms and the prospectus for buying corporate bonds over 25 million in value, he has to be cautious. This documentation should be approved by the Czech National Bank (CNB). It might include clauses that increase the risk of the bonds, like the issuer’s bankruptcy or repayment terms. Approval by the ČNB doesn’t consider the issuer’s risk profile or their ability to repay the bond properly.

- Investor has to pay extra attention to bonds with an issue value under 25 million. These aren’t regulated at all. The issuer doesn’t have to issue anything for regulatory reasons or ask anyone for permission. Basically, they just prepare materials as a sales tool to cover expected investor questions.

- Marketing materials use terms like „Guaranteed by the CNB“ and so on. Just because the CNB approved a bond issue doesn’t mean they endorse it; they only checked that the prospectus meets all legal requirements, giving investors enough info to make their own decisions. For private bond issues (limited to 150 investors) and public issues up to 1 million EUR (or the equivalent in CZK), there might not even be a prospectus!

A bond is an investment tool where you, the investor, get a fixed, limited profit, but you take on unlimited risk if the issuer goes bankrupt. It’s always better to be cautious and informed than to get swept up by tempting bond offers.

Investment Alternatives – higher profits, lower risks

If you’re looking for an investment with low risk and steady returns, Salutem Fund offers an attractive option. This fund for qualified investors mainly focuses on residential real estate in its portfolio, which tends to be more resistant to economic ups and downs and lets you earn returns from both sales and rental income.

- In its PIA share class, the fund offers investors an annual return of 6.3% – 7.0%, a return 6.3% even in case of lower fund performance

- Preferred returns are secured by the fund’s founders with their own capital in the VIA share class. Plus, the founders only start making money once the investors‘ claims—holders of the priority investment shares (PIA)—are satisfied. Currently, the ratio of VIA to PIA shares is about 8.5 to 1.

The fund’s stability is also due to its low debt; the fund’s total liabilities are only a third of its assets.

Compared to bond issuers, Salutem Fund is under stricter supervision and is required to publish its financial results.

The fund’s manager, TILLER, investment company, a.s., is obliged to publish the fund’s financial results quarterly. Along with that, the Salutem Fund is legally required to have its financial results audited. Salutem Fund chose Audit One s.r.o. as its auditor, a CLA Global member firm.

The Advantage of Compound Interest over Fixed Coupon Payments

Bondholders receive their returns regularly but cannot take advantage of compound interest. But with the Salutem Fund, boosting returns through compound interest is basically the main idea. For the PIA share class, this leads to returns of:

- 20.1% – 22.5% in 3 years

- 35.7% – 40.2% in 5 years

Moreover, if you hold PIA shares for over 3 years and then sell them, the sales up to 40 million CZK are tax-free for personal income tax, unlike bond interest, which gets a 15% withholding tax. A fund return of 6.3% per year is like getting a bond yield of 7.4%, and that’s not even counting the compound interest (before you file your tax return, you should check this with a tax advisor).

Flexible vs. Fixed Investment Horizon: A Comparative Analysis

The holding period for fund shares is unlimited, whereas the holding period for a bond is determined by its maturity date. Even if an investor want to keep getting interest payments, once the bond matures, he can’t. But with a fund, how long investor keeps shares is totally up to him and isn’t limited by time.

Investing in the Salutem Fund’s PIA share class represents a more advantageous alternative to purchasing bonds, both in terms of returns and risk.

Liquidity

As mentioned above, most people buying corporate bonds plan to keep them until they mature. If, for any reason, they need to sell them early, they often run into trouble since they don’t know who would buy them, and the bond issuer isn’t obligated to take them back.

With the Salutem Fund, however, the investor always has a guaranteed buyback of their shares, regardless of how long they’ve been holding them.

Overall Comparison of the Fund with Bonds

| Salutem Fund – PIA | Bond | |

| Guaranteed fixed return (over 1 year) | ✅ | ✅ |

| Liquid product (within 1 year) | ✅ | ❌ |

| No exit fees | ✅ | ✅ |

| No time commitment | ✅ | ❌ |

| No ongoing costs | ✅ | ✅ |

| Flexible investment horizon | ✅ | ❌ |

| Tax advantages | ✅ | ❌ |

| Level of security | High | Middle |

| Form of collateral/security | VIA share class | ❌ |

Investing in the Salutem Fund’s PIA share class is a more favorable alternative to buying bonds, both in terms of returns and risk.

Higher Returns with Salutem Fund

Salutem Fund also offers a PRIA share class, aiming for higher growth returns—though not guaranteed. The fund’s strategy is to achieve at least 15% per year, which would mean a 12.2% annual gain for an investor holding PRIA shares, and about 77.8% over 5 years.